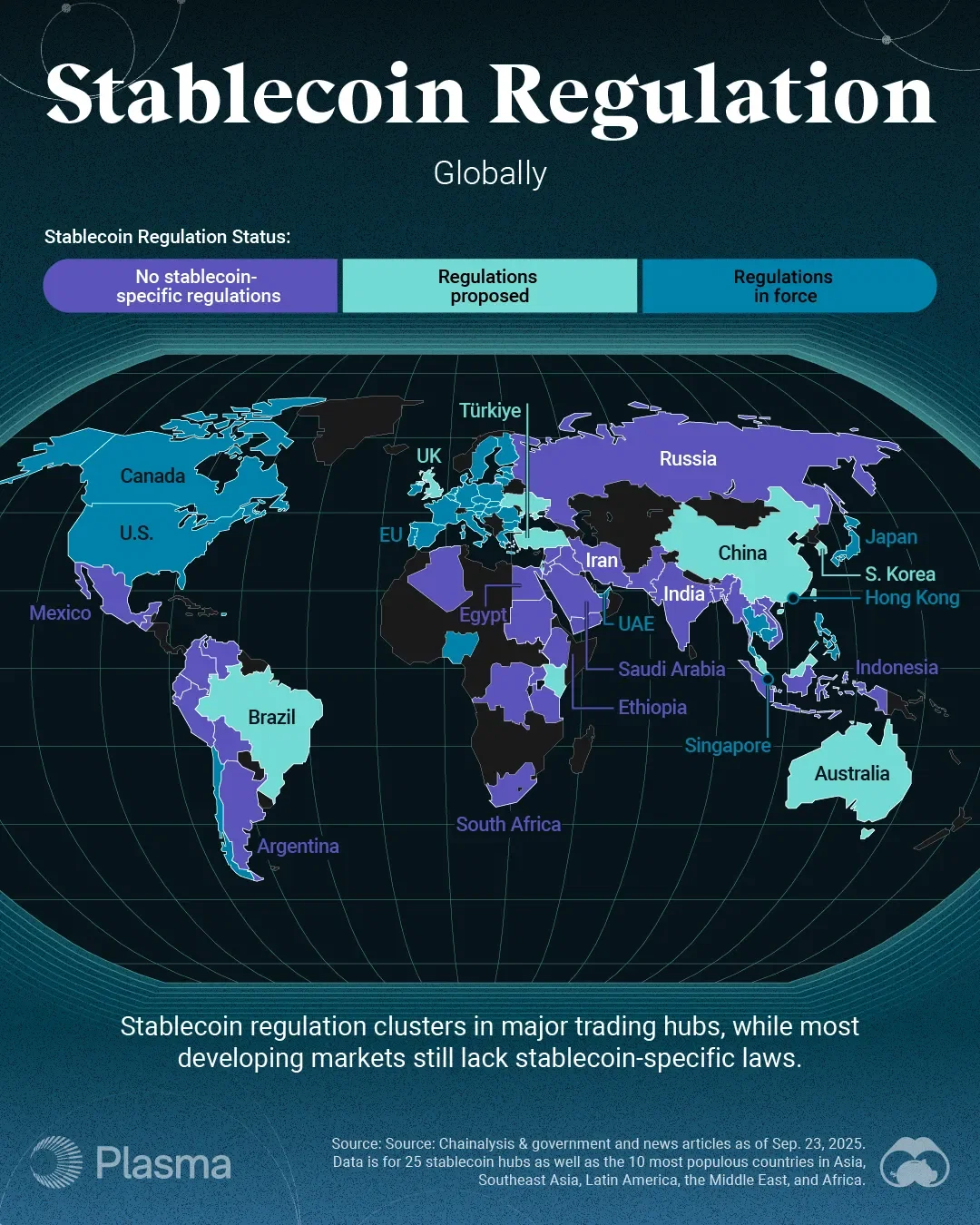

What stablecoin regulation 2026 means for issuers

The stablecoin regulatory landscape in 2026 is defined by two major frameworks: the US GENIUS Act, which establishes a federal payment stablecoin regime, and the EU’s MiCA, which provides comprehensive digital asset rules. Issuers are currently navigating the implementation phase of these laws.

Stablecoin issuers in 2026 operate within a dual-track regulatory environment. The United States and the European Union have established the primary frameworks governing digital dollar and euro issuers, respectively. This period marks the transition from legislative passage to active enforcement and rulemaking.

In the United States, the GENIUS Act was enacted on July 18, 2025. It creates a specific regulatory framework for payment stablecoin activities, primarily overseen by federal banking agencies. The Office of the Comptroller of the Currency (OCC) has since issued notices of proposed rulemaking to detail compliance requirements for issuers seeking to operate under this federal charter 1.

Simultaneously, the European Union’s Markets in Crypto-Assets (MiCA) regulation is fully in effect. MiCA provides a comprehensive set of rules for digital assets, including strict reserve requirements and transparency mandates for stablecoin issuers operating within the EU. Issuers must align their operations with these distinct but parallel regimes, depending on their target markets.

Reserve and redemption rules

The GENIUS Act establishes strict guardrails for how issuers hold backing assets and handle customer withdrawals. Under the proposed rules issued by the Treasury and the FDIC in early 2026, payment stablecoin issuers must maintain high-quality liquid assets to ensure immediate solvency. These reserve assets are largely restricted to cash and short-term U.S. Treasury securities, eliminating the riskier commercial paper or corporate bonds that plagued earlier models.

To protect the broader financial system, the legislation explicitly prohibits issuers from paying interest on stablecoin balances. This constraint prevents stablecoins from competing directly with bank deposits or government securities, a move designed to reduce monetary policy interference. While this limits yield opportunities for holders, it simplifies the regulatory classification by treating the token strictly as a payment instrument rather than an investment product.

Redemption timelines are equally rigid. The FDIC’s proposed rule requires issuers to redeem stablecoins within two business days of a customer request. This standard ensures that users can convert their digital tokens back into fiat currency without significant delay, maintaining the asset’s function as a stable medium of exchange. Issuers must also hold these reserves in segregated accounts, preventing commingling with corporate operating funds.

The GENIUS Act explicitly prohibits paying interest on payment stablecoins to mitigate monetary policy risks and prevent bank disintermediation.

These requirements apply to all federally permitted payment stablecoin issuers, including those regulated by the OCC, FDIC, and Federal Reserve. The Treasury’s proposed rule details how these entities must report reserve compositions, ensuring transparency for regulators and the public alike. By mandating strict reserve holdings and rapid redemption, the framework aims to restore trust in digital dollar equivalents while keeping them separate from traditional banking risks.

How MiCA Enforcement Shapes the EU Stablecoin Market

The European Union’s Markets in Crypto-Assets (MiCA) regulation moved from framework to active enforcement in 2026, fundamentally altering the operational landscape for stablecoin issuers. For Asset-Referenced Tokens (ARTs) and Electronic Money Tokens (EMTs), the rules are no longer theoretical; they are daily compliance requirements enforced by national competent authorities under the European Securities and Markets Authority (ESMA) oversight.

Strict Reserve and Governance Rules

MiCA imposes rigorous standards on ARTs and EMTs that go beyond traditional financial regulations. Issuers must maintain full backing of tokens by high-quality liquid assets, segregated from their own corporate funds. This segregation is critical: if an issuer faces insolvency, token holders have priority claims on the reserve assets. The regulation also mandates strict governance structures, requiring issuers to disclose reserve composition, auditing procedures, and redemption mechanisms transparently.

Cross-border passporting allows compliant issuers to operate across all EU member states with a single license from their home country’s regulator. This harmonization reduces fragmentation but increases the scrutiny on the primary licensing authority. In 2026, several major issuers have adjusted their legal structures to centralize compliance through entities in Ireland or Luxembourg, leveraging these jurisdictions’ established supervisory frameworks.

Interaction with US Regulatory Efforts

While the EU enforces MiCA, the United States remains without a comprehensive federal stablecoin law as of 2026. The GENIUS Act and similar legislative proposals have advanced in committees but lack final passage. This regulatory divergence creates a complex operational reality for global issuers. US-based entities often establish EU subsidiaries to access the single market, while EU issuers navigate US restrictions on offering services to American retail customers.

The lack of US federal clarity contrasts sharply with the EU’s detailed implementation. State Street and other institutional observers note that this gap influences capital flows, with institutional stablecoin reserves increasingly favoring EU-compliant structures for their legal certainty. However, the absence of a US equivalent means cross-border interoperability remains a technical and legal challenge rather than a standardized feature.

Enforcement Timeline and Recent Actions

The enforcement trajectory has been aggressive. Initial licensing rounds concluded in late 2025, with ESMA publishing guidance on reserve asset quality and operational resilience in early 2026. National authorities have begun conducting on-site inspections of ART and EMT issuers, focusing on reserve verification and redemption processes. Non-compliance carries significant penalties, including fines and potential revocation of licenses.

This structured enforcement distinguishes the EU approach from the more fragmented US state-level regulatory environment. For market participants, the EU’s path offers predictability, even if it demands higher initial compliance costs. The focus remains on consumer protection and financial stability, with MiCA serving as the primary regulatory instrument.

US and EU stablecoin frameworks compared

The United States and European Union have taken divergent paths in regulating stablecoins, reflecting different priorities in financial stability and consumer protection. The US approach, anchored by the GENIUS Act enacted in July 2025, focuses on a federal licensing regime for payment stablecoins, while the EU’s Markets in Crypto-Assets (MiCA) regulation, fully applicable since 2024, imposes a unified passporting system across member states.

The structural differences are most visible in reserve requirements and issuer eligibility. The US framework emphasizes strict reserve backing by liquid assets, primarily cash and short-term Treasuries, to ensure immediate redeemability. In contrast, MiCA distinguishes between asset-referenced tokens and e-money tokens, with the latter subject to stricter reserve rules similar to traditional e-money institutions. The EU also mandates a more granular disclosure of reserve composition and regular audits by independent third parties.

Consumer protection mechanisms further highlight the split. The US model relies on the OCC and other federal regulators to enforce compliance, with a focus on preventing systemic risk. The EU model, however, provides a direct right of redemption for holders and requires issuers to maintain a ring-fenced reserve account, ensuring that consumer funds are protected even if the issuer faces insolvency.

Compliance checklist for stablecoin issuers

Issuers must align their operations with the GENIUS Act and MiCA frameworks to maintain legal standing. The following steps outline the core requirements for reserve management, redemption, and reporting.

Hold reserve assets in segregated accounts at qualifying financial institutions. The OCC’s proposed rule (March 2026) specifies strict eligibility criteria for these assets, prioritizing cash and short-term U.S. Treasuries to minimize liquidity risk.

Establish infrastructure to process redemption requests within two business days. The FDIC’s April 2026 notice confirms this timeline for Payment-Producing Stablecoin Issuers (PPSIs), ensuring users can convert tokens to fiat without operational delays.

Release monthly attestation reports from an independent third-party auditor. These reports must verify the total value of reserve assets matches the outstanding stablecoin supply, providing transparency to regulators and the public.

Integrate Travel Rule standards into transaction monitoring systems. Issuers must collect and transmit originator and beneficiary information for transfers exceeding regulatory thresholds, aligning with FATF guidelines and MiCA requirements.

Complete registration with the OCC, FDIC, or state regulators depending on your charter. Ensure all corporate governance documents reflect the new regulatory expectations for stablecoin issuance and reserve management.

Frequently asked questions about 2026 rules

How does the GENIUS Act differ from MiCA regarding reserve assets?

The GENIUS Act restricts payment stablecoin reserves primarily to cash and short-term U.S. Treasury securities to ensure immediate liquidity and safety. MiCA allows for a broader range of high-quality liquid assets for Asset-Referenced Tokens (ARTs) but imposes stricter segregation and auditing requirements for Electronic Money Tokens (EMTs) that mirror traditional e-money institutions.

Can US issuers operate in the EU under the GENIUS Act?

No. The GENIUS Act is a US federal law. To operate in the EU, issuers must comply with MiCA and obtain a license from an EU national competent authority. Many US-based issuers establish separate EU subsidiaries to meet these requirements.

What happens if a stablecoin issuer fails to redeem tokens within two days?

Under the FDIC’s proposed rules linked to the GENIUS Act, failure to redeem within two business days constitutes a compliance violation. Issuers face potential fines, enforcement actions, and revocation of their federal charter. MiCA imposes similar strict timelines for EMTs, with penalties determined by national authorities.

Do stablecoin issuers pay interest on tokens in 2026?

No. The GENIUS Act explicitly prohibits paying interest on payment stablecoins to prevent competition with bank deposits and mitigate monetary policy risks. MiCA also generally prohibits interest-bearing features for EMTs to maintain their status as a medium of exchange rather than an investment product.

No comments yet. Be the first to share your thoughts!