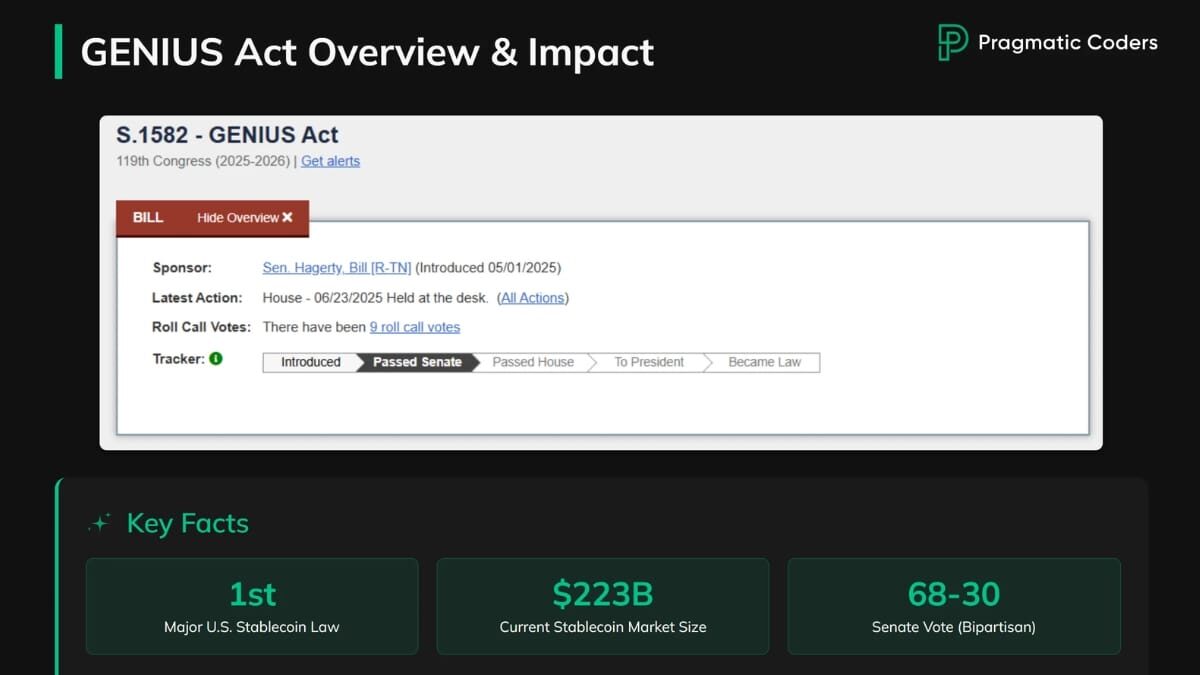

Stablecoins have been at the heart of crypto’s mainstream ambitions, but until 2025, the U. S. lacked a unified federal framework. That changed with the GENIUS Act, signed into law on July 18,2025. This landmark legislation introduces a sweeping set of rules for stablecoin issuers, from licensing and reserves to consumer protection and compliance reporting. If you’re a legal advisor, compliance lead, or crypto founder, understanding the GENIUS Act isn’t just helpful, it’s essential for operating in the U. S. digital asset space.

GENIUS Act Stablecoin Regulation: What’s New in U. S. Law?

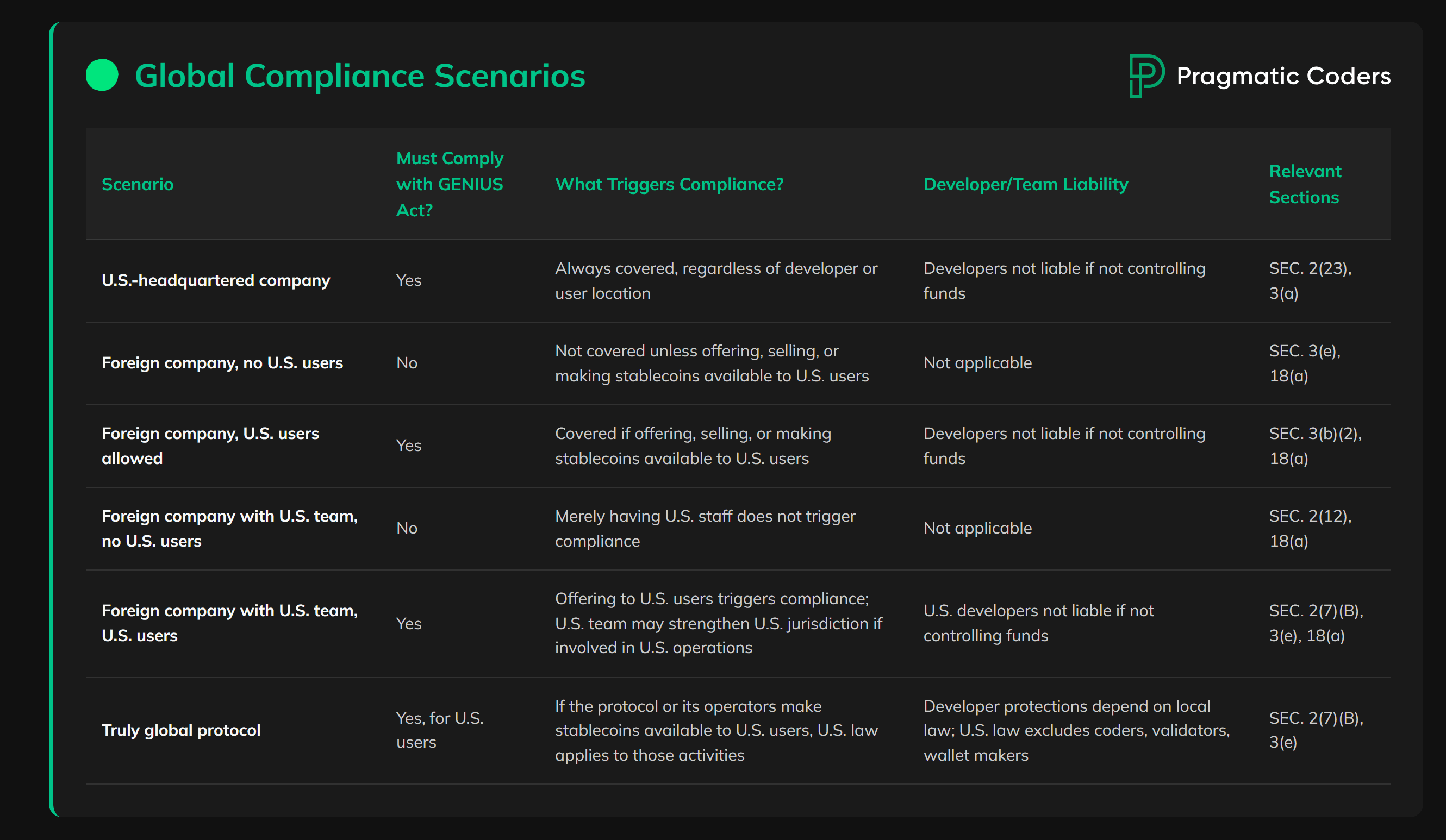

The GENIUS Act is the first federal law to set clear standards for payment stablecoins in the United States. Unlike previous patchwork state regimes, it creates a dual system: large issuers face direct federal oversight while smaller players can opt into state supervision if their state’s rules are deemed “substantially similar. ”

Key takeaways from the Act include:

- 100% Reserve Backing: All stablecoins must be backed 1: 1 by high-quality liquid assets like U. S. dollars or short-term Treasuries.

- Issuer Licensing: Only permitted payment stablecoin issuers (PPSIs) can issue stablecoins, this includes bank subsidiaries, licensed non-banks, and qualified foreign entities.

- Consumer Protections: Reserve assets are bankruptcy-remote and holders have priority claims if an issuer fails.

This law marks a decisive shift toward mainstream adoption by giving both consumers and institutions confidence that stablecoins are safe, fully backed, and well-regulated. For more detail on how these rules affect your business or clients, see GENIUS Act Explained: What the 2025 U. S. Stablecoin Law Means for Compliance.

Stablecoin Issuer Licensing: Who Can Issue Under the GENIUS Act?

The Act doesn’t just let anyone launch a dollar-pegged token overnight. To issue payment stablecoins in 2025 and beyond, entities must qualify as PPSIs under one of three categories:

Key Permitted Stablecoin Issuers Under the GENIUS Act

- Insured Depository Institution Subsidiaries: These are subsidiaries of federally insured banks and credit unions, authorized to issue payment stablecoins under direct federal oversight. Their parent institutions are regulated by agencies like the FDIC and OCC.

- Nonbank Entities with Federal Licenses: Nonbank companies that obtain a special stablecoin issuer license from a federal regulator (such as the OCC or Federal Reserve) can issue payment stablecoins, provided they meet all reserve, compliance, and reporting requirements.

- Nonbank Entities with Certified State Licenses: Nonbank issuers with a state license may issue stablecoins if their state's regulatory regime is certified as "substantially similar" to federal standards. Issuers with $10 billion or less in outstanding stablecoins may remain under state supervision.

- Qualified Foreign Issuers: Foreign companies may issue payment stablecoins in the U.S. if they meet GENIUS Act standards and receive approval from U.S. regulators, ensuring compliance with all reserve and consumer protection requirements.

- Transitioning Decentralized or Anonymous Issuers: Existing decentralized or anonymous stablecoin issuers are given a three-year window to achieve full compliance and obtain the necessary licensing to continue operating legally in the U.S.

If you’re an existing decentralized or anonymous issuer (think legacy DeFi protocols), you have a three-year window to come into compliance, either by restructuring your operations or partnering with a licensed entity.

Larger issuers, those with over $10 billion in outstanding tokens, are supervised by federal agencies like the OCC, Federal Reserve Board, and FDIC. Smaller issuers (under $10 billion) can remain under state regulation if their state framework meets federal standards.

Reserve Requirements and Audit Compliance: The Backbone of Trust

The heart of stablecoin reserve requirements is simple but strict: every token must be backed by an equivalent dollar value held in bankruptcy-remote accounts. Permitted reserves include U. S. currency, insured demand deposits at banks, short-term (<93 days) Treasury securities, and select overnight repo agreements.

No more creative accounting or risky rehypothecation. With only narrow exceptions for liquidity management (and only with regulatory approval), reserve assets can’t be lent out or leveraged elsewhere.

PPSIs must publish monthly reserve reports detailing asset composition and total value, verified by independent third-party attestations, and submit annual audited financial statements. Enhanced oversight kicks in once an issuer surpasses $50 billion in market cap. For practical guidance on meeting these requirements as an issuer or compliance officer, check out GENIUS Act Explained: New Stablecoin Licensing and Audit Requirements in the US (2025).

Beyond reserves and licensing, the GENIUS Act stablecoin regulation sets a new bar for transparency and risk management. Issuers must not only prove solvency, but also maintain robust anti-money laundering (AML) and know-your-customer (KYC) programs on par with traditional financial institutions. This means ongoing customer identity verification, transaction monitoring, and mandatory reporting of suspicious activities to FinCEN.

Consumer Protections: What Happens If an Issuer Fails?

Arguably one of the most significant shifts is how the Act addresses consumer risk in case an issuer goes under. Under these rules, reserve assets are legally separated from the issuer’s own funds. If a PPSI enters bankruptcy, stablecoin holders have priority claims: meaning their tokens are directly backed by actual dollars or Treasuries in segregated accounts, not just a vague promise.

- Bankruptcy-remote reserves: Holders’ funds are shielded from other creditors if an issuer fails.

- No commingling: Reserve assets cannot be mixed with operational funds or used for risky investments.

- Priority payout: Stablecoin users are first in line to recover their assets during insolvency proceedings.

This structure is designed to prevent another Terra/Luna-style collapse, giving both retail users and institutional investors confidence that their digital dollars are truly safe. For more on consumer safeguards and bankruptcy protections under this law, see How the New US Stablecoin Law Impacts Issuers, Banks, and DeFi.

Compliance Timelines and Ongoing Obligations: What’s Next for Issuers?

The GENIUS Act provides a transition period for existing issuers to come into compliance. Decentralized projects have up to three years to meet licensing and reserve requirements or face enforcement actions. For new entrants, all obligations apply immediately upon launch.

GENIUS Act Stablecoin Issuer Reporting Deadlines

- Monthly Reserve Reports: Issuers must publish detailed reserve reports by the 15th of each month, disclosing the composition and total value of all backing assets. Each report must be verified by an independent third-party attestation to ensure transparency and compliance.

- Annual Audited Financial Statements: By March 31st each year, stablecoin issuers must submit audited financial statements for the previous fiscal year. These audits must be conducted by a registered independent public accounting firm and include disclosures on reserve management and risk controls.

- Suspicious Activity Reports (SARs): Under the Bank Secrecy Act, issuers are required to file SARs with FinCEN within 30 days of detecting suspicious activity related to money laundering or fraud. This is an ongoing obligation, not tied to a specific calendar date.

- Enhanced Oversight for Large Issuers: Issuers with over $50 billion in market capitalization must comply with additional annual oversight and reporting requirements as specified by federal regulators. This includes more frequent risk assessments and regulatory reviews.

- Timely Disclosure of Material Events: Issuers must promptly report any material changes—such as significant reserve composition shifts or cybersecurity incidents—to regulators and the public, typically within 72 hours of discovery.

PPSIs must stay vigilant with ongoing regulatory filings, monthly reserve attestations, annual audits, and real-time AML/KYC monitoring aren’t optional add-ons; they’re core requirements. Non-compliance can result in license revocation or civil penalties.

Looking Ahead: The U. S. as a Global Stablecoin Hub?

The GENIUS Act isn’t just about domestic oversight, it positions the U. S. as a global leader in digital asset regulation by setting clear expectations for foreign issuers seeking access to American markets. As other jurisdictions watch closely (and some prepare copycat laws), U. S. -based stablecoins may become the gold standard for trust and transparency worldwide.

If you’re preparing your compliance roadmap or advising clients on cross-border issuance strategies, you’ll want to keep tabs on evolving interpretations of “substantially similar” state frameworks and potential updates from federal agencies. For deeper dives into practical steps for compliance teams, including sample policies and audit checklists, explore our latest resources:

- GENIUS Act Explained: US Stablecoin Licensing and Audit Rules (2025)

- What US Stablecoin Issuers Need To Know For Compliance

The bottom line? The GENIUS Act brings both clarity and accountability to stablecoins operating at scale in America, raising the bar for reserve management, consumer protection, and regulatory transparency as we move toward mainstream adoption of digital dollars.

No comments yet. Be the first to share your thoughts!