The U. S. regulatory landscape for stablecoins has fundamentally shifted with the passage of the Guiding and Establishing National Innovation for U. S. Stablecoins (GENIUS) Act on July 18,2025. This landmark legislation, signed into law by President Donald Trump, delivers long-awaited clarity for digital asset participants and sets a rigorous new standard for compliance, risk management, and transparency. For legal professionals, crypto businesses, banks, and fintech innovators, understanding the GENIUS Act's requirements is now mission-critical.

GENIUS Act: Key Provisions Redefining U. S. Stablecoin Regulation

The GENIUS Act targets payment stablecoins, digital tokens pegged to assets like the U. S. dollar, by establishing a comprehensive federal framework that covers who can issue them, how reserves must be managed, and what compliance protocols are mandatory. The act’s most impactful features include:

GENIUS Act Stablecoin Issuer Requirements

- Permitted Payment Stablecoin Issuer (PPSI) Status: Only entities classified as PPSIs—such as subsidiaries of insured depository institutions, nonbanks with state or federal licenses, and qualified foreign issuers—may issue payment stablecoins in the U.S. Non-financial firms are generally excluded unless granted unanimous approval by the Stablecoin Certification Review Committee (SCRC).

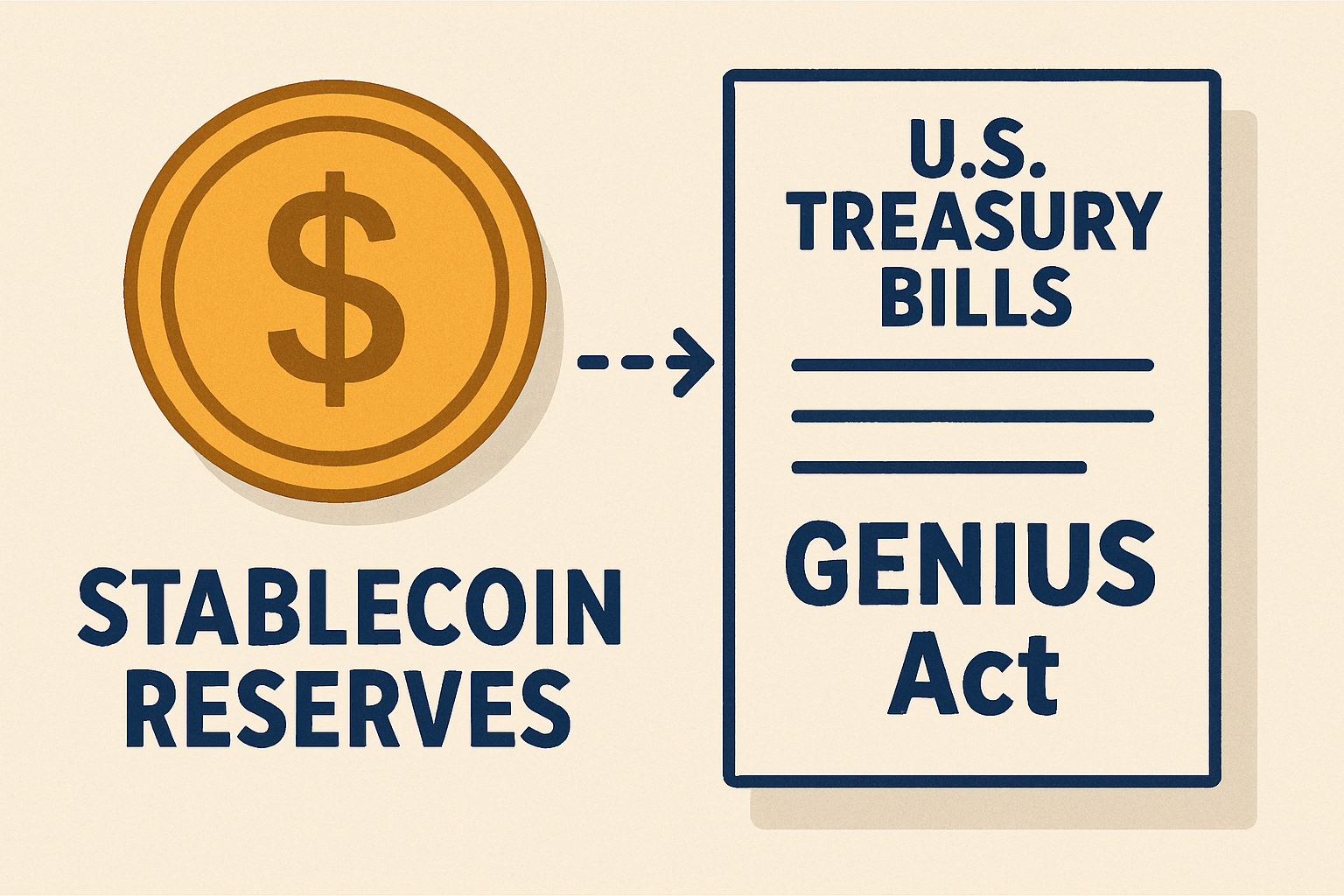

- 1:1 Reserve Backing and Segregation: Issuers must maintain reserves equal to the value of all outstanding stablecoins, held in bankruptcy-remote accounts and backed by high-quality, liquid assets like U.S. dollars, Treasury bills, overnight repos, demand deposits, and registered government money market funds.

- Monthly Public Disclosures: Stablecoin issuers are required to publish monthly reports detailing the composition of their reserves, enhancing transparency and consumer confidence.

- Third-Party Reserve Attestations and Audits: All issuers must obtain monthly attestations of reserves from independent auditors. Issuers with over $10 billion in outstanding stablecoins are subject to annual audits and enhanced federal oversight.

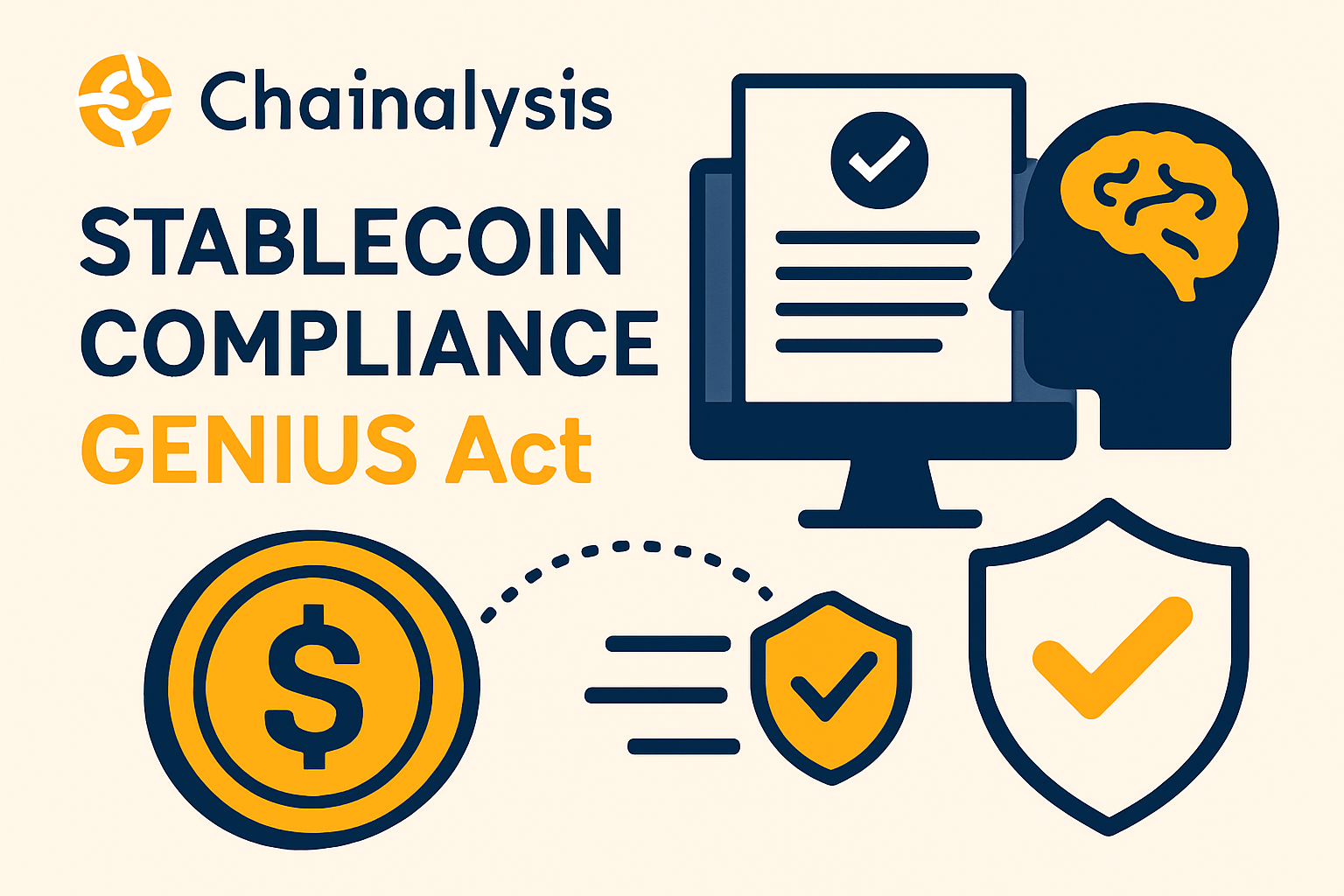

- Robust AML and Sanctions Compliance: Issuers must implement comprehensive anti-money laundering (AML) and sanctions compliance programs, including customer due diligence and transaction monitoring, to align with federal standards.

- Operational and Reporting Upgrades: The Act requires issuers to strengthen financial controls, risk management, and reporting systems to meet new regulatory standards, which may increase operational costs but provide greater legitimacy and market access.

At the heart of the law is a strict licensing regime. Only permitted payment stablecoin issuers (PPSIs) may issue payment stablecoins in the U. S. , with eligibility limited to:

- Subsidiaries of insured depository institutions

- Nonbanks holding state or federal licenses

- Qualified foreign issuers meeting U. S. standards

Non-financial firms are generally excluded from issuing stablecoins unless they secure unanimous approval from a new oversight body, the Stablecoin Certification Review Committee (SCRC). This restriction targets large tech companies and other non-bank entities seeking entry into the rapidly growing U. S. stablecoin market.

Reserve Backing, Transparency, and Audit Requirements

The GENIUS Act's reserve requirements are among the most stringent globally. Issuers must maintain full 1: 1 reserves in bankruptcy-remote accounts, backed by high-quality liquid assets such as U. S. dollars, Treasury bills, overnight repos, demand deposits, or shares in registered government money market funds. This is designed to eliminate run risk and ensure holders can always redeem their coins at par value.

Transparency is not optional: monthly public disclosures of reserve compositions are now mandatory for all PPSIs. Additionally, third-party attestations of reserves must be conducted each month; issuers with more than $10 billion outstanding face annual audits and increased federal scrutiny.

Compliance Burden: AML Programs and Operational Implications

Beyond reserves, the GENIUS Act mandates robust anti-money laundering (AML) controls and sanctions screening across all PPSIs. Issuers must implement comprehensive customer due diligence processes and transaction monitoring systems to detect suspicious activity, a significant operational lift for both legacy financial institutions and crypto-native players.

This regulatory clarity comes at a cost: compliance upgrades will drive up operational expenses for both existing issuers and new entrants. Many industry participants are already investing in enhanced financial controls and reporting mechanisms to meet these heightened standards.

The new rules also impact accounting treatment, payment stablecoins issued by PPSIs are no longer classified as cash or cash equivalents under U. S. accounting standards. This subtle but important change affects how businesses report holdings on their balance sheets.

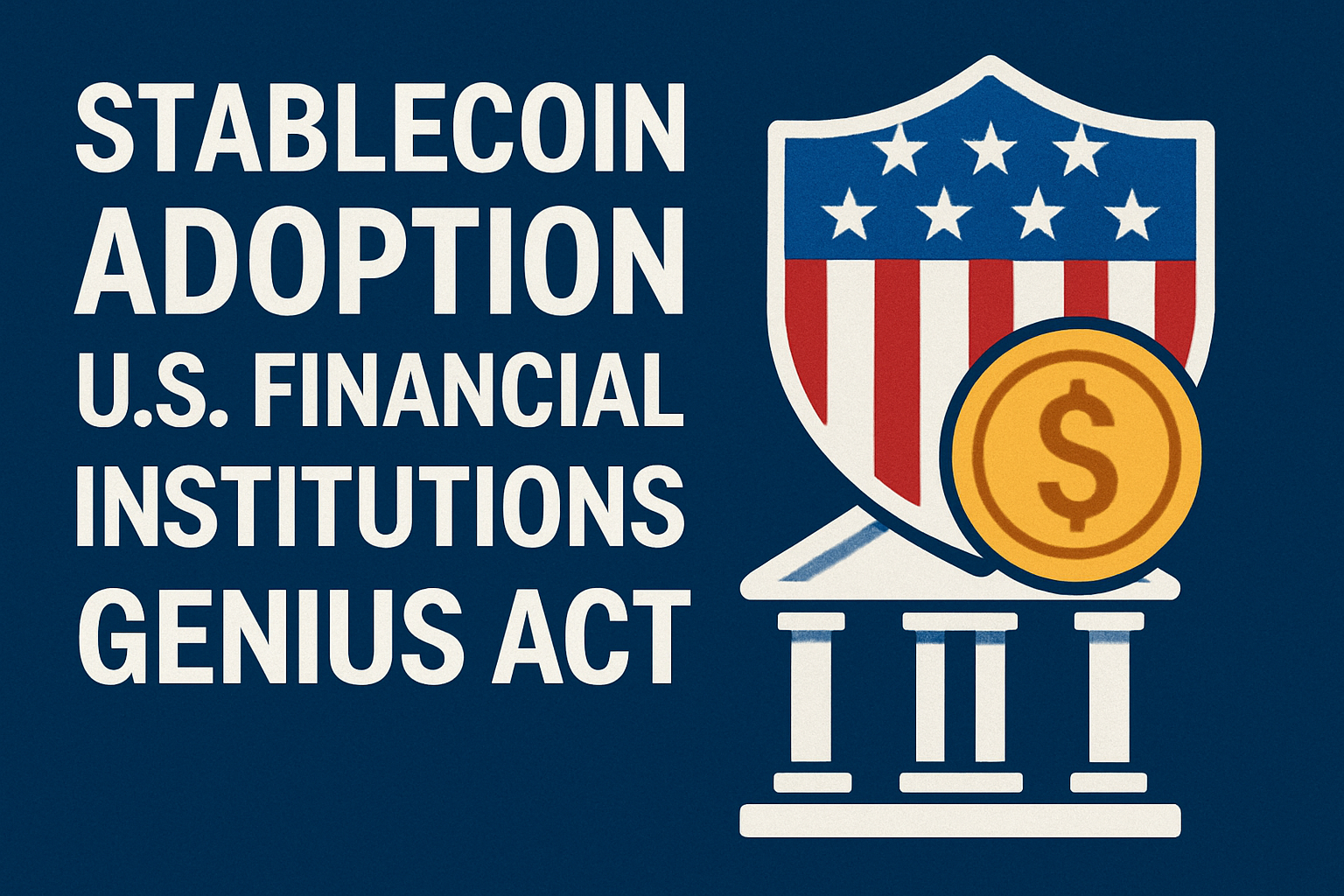

Paving the Way for Mainstream Stablecoin Adoption?

By enforcing strict reserve backing and transparency requirements while clarifying who may issue stablecoins in the United States, the GENIUS Act paves the way for greater institutional participation and mainstream adoption. Banks now have clear guidance to launch compliant stablecoin products; startups can seek state or federal licensure; investors gain confidence knowing that consumer protections are enshrined in law.

For a deeper dive into issuer eligibility rules and reserve mechanics under the new regime, see GENIUS Act Explained: What US Stablecoin Issuers Need to Know About 1: 1 Backing, Licensing and Compliance (2025 Update).

While the GENIUS Act sets a high bar for compliance, it also marks a turning point for U. S. stablecoin legitimacy. The law’s focus on transparency, consumer protection, and financial stability is already reshaping how institutions approach digital asset strategy. For many banks and fintechs, the new framework means stablecoin initiatives can finally move from pilot to production without lingering regulatory uncertainty.

However, the operational and legal lift should not be underestimated. Monthly reserve attestations, annual audits for large issuers, and comprehensive AML regimes require significant investment in compliance infrastructure. This is especially true for nonbank entities that must now meet standards on par with traditional financial institutions. The GENIUS Act’s explicit exclusion of most non-financial firms from stablecoin issuance also narrows the competitive landscape, potentially keeping Big Tech at arm’s length unless they clear the SCRC’s unanimous approval hurdle.

Business Adoption: New Opportunities and Strategic Shifts

With regulatory clarity comes a wave of business model innovation. U. S. banks are already exploring stablecoin-powered payment rails and treasury management tools, leveraging their existing compliance operations to gain first-mover advantage. Meanwhile, crypto-native firms face a strategic choice: invest in the robust controls needed to become a PPSI or pivot toward partnerships with licensed banks and trust companies.

Key Impacts of the GENIUS Act on U.S. Stablecoin Business Adoption

- Clear Regulatory Pathway for Banks and Licensed Entities: The GENIUS Act restricts stablecoin issuance to permitted payment stablecoin issuers (PPSIs), including subsidiaries of insured depository institutions and licensed nonbanks. This regulatory clarity enables established financial institutions like JPMorgan Chase and Circle to confidently develop and expand stablecoin products within a defined legal framework.

- Mandatory 1:1 Reserve Backing and Monthly Disclosures: Issuers must maintain bankruptcy-remote, 1:1 reserves in high-quality liquid assets such as U.S. Treasury bills and government money market funds. Monthly public disclosures and third-party attestations are now required, driving product development toward greater transparency and consumer trust.

- Enhanced Compliance and AML Standards: The Act mandates robust anti-money laundering (AML) and sanctions compliance programs, including customer due diligence and transaction monitoring. This raises the bar for compliance infrastructure, prompting stablecoin issuers to invest in advanced regtech solutions and partner with established compliance providers like Chainalysis and Elliptic.

- Higher Operational Costs and Barriers to Entry: The GENIUS Act's stringent compliance, reserve, and audit requirements increase operational costs for both new and existing issuers. Smaller startups may face challenges meeting these standards, potentially leading to industry consolidation among established players such as Circle and Paxos.

- Limited Entry for Non-Financial Firms: Non-financial companies, including major tech firms, are generally barred from issuing stablecoins unless they secure unanimous approval from the Stablecoin Certification Review Committee (SCRC). This restriction curtails the ability of companies like Meta (formerly Facebook) to launch proprietary stablecoins, shaping the competitive landscape.

- Boosted Investor and Consumer Confidence: By providing regulatory certainty and emphasizing transparency, consumer protection, and financial stability, the GENIUS Act encourages broader adoption of stablecoins by mainstream financial institutions and enterprises, paving the way for innovative payment and treasury solutions.

For global players, the GENIUS Act’s interoperability provisions, allowing qualified foreign issuers to participate if they meet U. S. standards, may set a template for cross-border stablecoin frameworks. This could accelerate international adoption while reinforcing the dollar’s digital primacy.

Still, questions remain about how state regulators will interact with the federal regime and how quickly new PPSI applications will be processed. Market participants should expect ongoing regulatory guidance and possible amendments as implementation unfolds.

What Comes Next for Stablecoin Regulation?

The GENIUS Act’s passage is just the opening chapter for U. S. stablecoin regulation. Legal teams and compliance officers should closely monitor rulemaking from federal agencies as they flesh out technical requirements and enforcement protocols. Early engagement with regulators and third-party auditors will be critical to ensure ongoing compliance and minimize disruption.

For further analysis on licensing implications and regulatory timelines under the new law, see GENIUS Act Explained: US Stablecoin Licensing, Reserve and Audit Rules (2025).

Bottom line: The GENIUS Act is a double-edged sword, demanding unprecedented transparency and oversight but finally unlocking mainstream adoption for compliant issuers. The winners will be those who can adapt quickly, build trust through rigorous controls, and seize new opportunities in a regulated digital dollar economy.

No comments yet. Be the first to share your thoughts!