The stablecoin landscape has entered a new era in 2025, as regulatory clarity from both sides of the Atlantic begins to reshape the way global merchants engage with digital assets. The passage of the U. S. GENIUS Act and the full implementation of the EU’s Markets in Crypto-Assets Regulation (MiCA) have created a dual axis of compliance that is rapidly influencing payment flows, merchant adoption, and cross-border operations. For businesses seeking to leverage stablecoins for speed, efficiency, and cost savings, understanding these frameworks is now a prerequisite for legal operation and sustainable growth.

GENIUS Act: The U. S. Sets a New Bar for Stablecoin Compliance

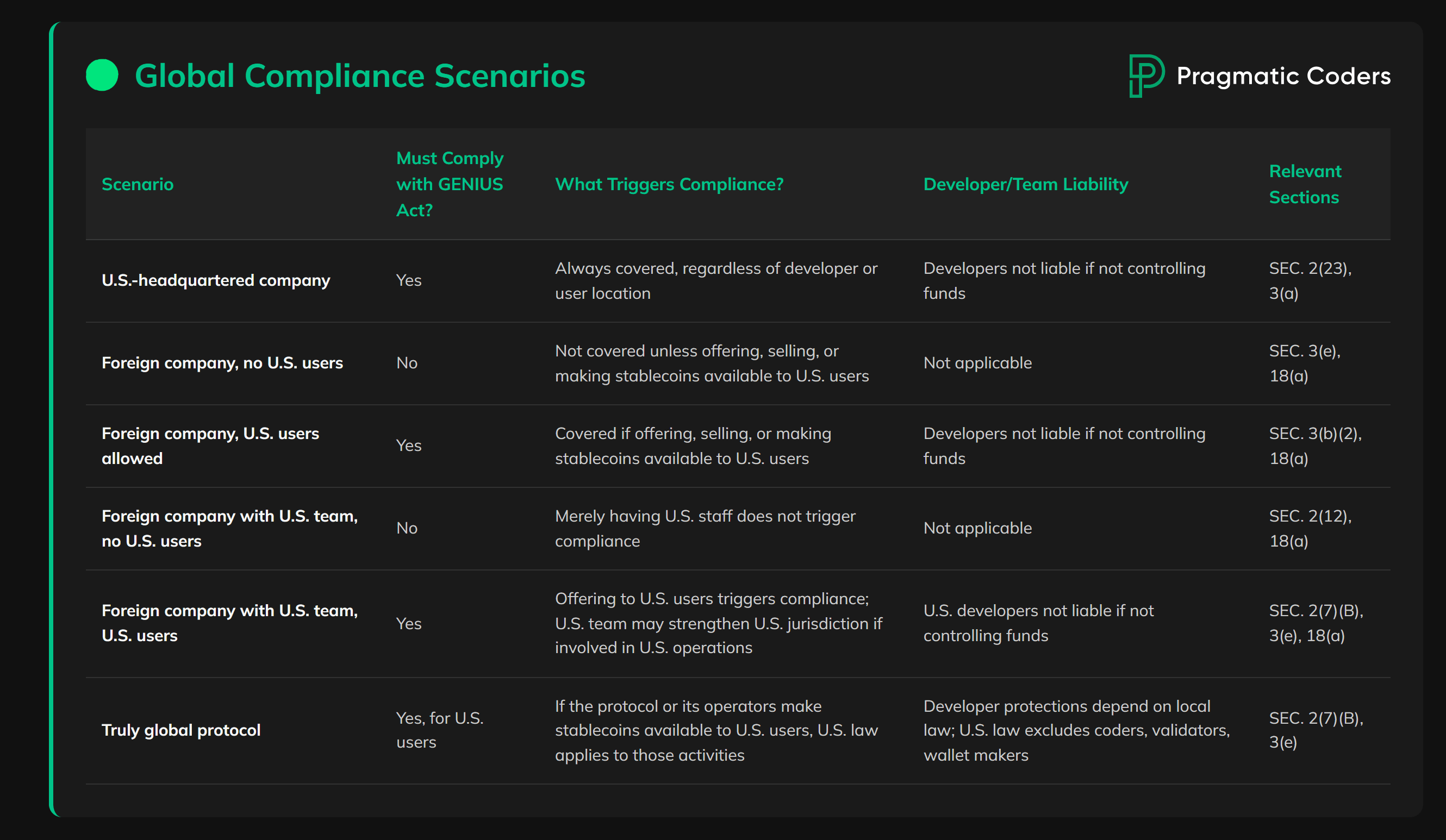

Signed into law in July 2025, the Guiding and Establishing National Innovation for U. S. Stablecoins (GENIUS) Act represents America’s first comprehensive federal legislation dedicated to digital assets. This bipartisan milestone establishes strict criteria for payment stablecoin issuers:

- Full Reserve Backing: Every stablecoin must be backed 1: 1 by U. S. dollars held in segregated accounts.

- Federal Licensing: Issuers are required to secure a federal banking charter, subjecting them to oversight on par with traditional financial institutions.

- Audit Transparency: Regular third-party audits must be published, providing assurance on reserve sufficiency and operational soundness.

- AML and amp; Consumer Protections: Enhanced anti-money laundering protocols and consumer safeguarding measures are now mandatory.

This framework is designed to legitimize stablecoins as an integral bridge between traditional finance and crypto payments. Only entities meeting these criteria can legally issue payment stablecoins in the U. S. , effectively excluding unregulated or algorithmic tokens from mainstream commerce. The result is an environment where merchants can accept compliant stablecoins with confidence that they meet robust standards for solvency and transparency.

MiCA: Europe’s Blueprint for Digital Asset Regulation

While the GENIUS Act brings overdue clarity to U. S. markets, MiCA has already set a high bar across Europe since December 2024. MiCA classifies stablecoins as either electronic money tokens (EMTs) or asset-referenced tokens (ARTs), each subject to its own licensing regime:

- Issuer Licensing and amp; Reserves: All issuers must be licensed within an EU member state and maintain liquid reserves matching their outstanding token supply.

- Redemption Rights and amp; Transparency: Merchants benefit from clear redemption processes and regular public audits, requirements that have led major exchanges to delist non-compliant tokens.

- KYC/AML Alignment: Stringent Know Your Customer (KYC) and AML checks are now standard across European payment flows involving stablecoins.

The harmonization under MiCA has catalyzed a rapid shift toward regulated tokens like USDC, payment volumes surged by an impressive 337% in H1 2025 compared to last year according to industry data. Merchants operating across borders are increasingly prioritizing MiCA-compliant assets to ensure seamless access to European customers without regulatory risk.

The Merchant Perspective: Adapting Payment Infrastructure for Regulatory Certainty

The dual rollout of GENIUS Act and MiCA means global merchants can no longer rely on informal or lightly regulated digital assets if they wish to scale operations lawfully in key markets. Instead, forward-looking businesses are adopting several core strategies:

- Selecting Compliant Stablecoins: Only those that meet both U. S. federal standards and EU licensing requirements are now viable for large-scale commerce.

- Upgrading Compliance Protocols: Enhanced KYC/AML processes, often automated through partnerships with regulated payment processors, are becoming standard practice.

- Leveraging Transparent Providers: Preference is given to issuers who publish frequent audit reports and offer clear redemption mechanisms, reducing counterparty risk.

This compliance-first approach isn’t just about avoiding penalties, it’s about unlocking new customer segments who demand trustworthiness from digital payments providers. As regulatory scrutiny intensifies globally, merchants who align early with GENIUS Act- or MiCA-compliant solutions will be best positioned for growth as digital asset commerce becomes mainstream.

If you want deeper technical guidance on these frameworks or practical steps for merchant integration, see our extended breakdown at How the GENIUS Act and MiCA Are Reshaping Stablecoin Compliance in 2025.

Another key implication of these regulatory shifts is the narrowing window for arbitrage between jurisdictions. Previously, merchants could route payments through less-regulated stablecoins to minimize friction or cost. Today, with both the GENIUS Act and MiCA imposing similar standards, full reserve backing, licensing, and mandatory disclosures, regulatory arbitrage is rapidly disappearing. This convergence is driving a global baseline for stablecoin quality, benefiting both merchants and end-users with greater reliability and lower risk of sudden asset de-listings.

Cross-border payments are also seeing tangible improvements. Merchants using compliant stablecoins can now move value between the U. S. and EU markets with reduced settlement times and fewer compliance headaches. As payment processors integrate these standards into their platforms, cross-jurisdictional commerce becomes more seamless, provided that merchants select tokens which meet both sets of rules. This efficiency translates into faster checkouts, higher transaction success rates, and improved customer satisfaction.

Risks and Opportunities: Navigating the New Stablecoin Compliance Landscape

Despite the benefits, the new era of regulation introduces challenges that merchants must address head-on:

- Onboarding Complexity: The process for onboarding new payment providers or wallets is now more rigorous due to KYC/AML checks mandated by both frameworks.

- Operational Adjustments: Merchants must allocate resources to ongoing compliance monitoring as audit cycles become more frequent and regulators increase oversight.

- Token Selection Risks: Choosing non-compliant or borderline tokens can result in sudden loss of payment channels if issuers are delisted or fined.

The upside? Compliant merchants gain access to a wider pool of institutional partners, banks, fintechs, and large enterprises, that previously hesitated due to regulatory uncertainty. This creates new opportunities for B2B payments, payroll disbursements in digital dollars or euros, loyalty programs denominated in stablecoins, and even programmable money use cases that leverage smart contracts for automatic settlement.

The GENIUS Act’s requirement for regular public audits has already led to increased transparency from leading issuers. For example, monthly reserve attestations have become industry standard among top U. S. -based stablecoin providers. Similarly, MiCA’s insistence on clear redemption rights means European customers can convert tokens back to fiat at par value without hidden fees, a major step up from previous practices.

What’s Next? The Road Ahead for Merchant Stablecoin Adoption

The pace of regulatory harmonization suggests that other regions will soon follow suit. The UK’s Financial Services and Markets Act amendments are expected to mirror core elements of MiCA by late 2026, while Canada is already piloting federal licensing for digital asset issuers. Merchants with global ambitions should monitor these developments closely, and prioritize adaptable infrastructure that supports multi-jurisdictional compliance from day one.

Ultimately, those who invest early in robust compliance protocols will be best positioned as digital asset payments move from niche innovation to mainstream utility. The GENIUS Act and MiCA are not just legal hurdles, they are catalysts accelerating merchant trust in stablecoins as a core part of the payments stack.

If you’re evaluating your next steps or want a side-by-side breakdown of U. S. , EU, UK, and Canadian approaches this year, our deep dive at GENIUS Act and Global Stablecoin Regulation: How the US, EU, UK and Canada Are Setting New Compliance Standards for 2025 offers detailed analysis tailored for legal teams and operational leads.

No comments yet. Be the first to share your thoughts!